Understanding Capital Gains Taxes

Capital gains taxes are the toll you pay when you make a profit from selling an investment such as stocks, bonds, or real estate. They represent the government’s share of your success — even though, as many investors say, “Uncle Sam takes no risk, yet always gets paid.”

To put it simply, a capital gain occurs when you sell an asset for more than you paid for it. The difference between the purchase price and the selling price is your gain, and that gain is subject to taxation.

Whether you’re a new investor just starting out or a seasoned trader, understanding how these taxes work can make a major difference in how much profit you keep. For a deeper understanding of how stock value plays into your taxable gains, check out Understanding the Real Value of a Stock.

Why Capital Gains Taxes Matter

Many investors underestimate the impact of taxes on their returns. Imagine turning a $10,000 investment into $15,000 — that’s a $5,000 gain. Without planning, a large portion of that gain could go to taxes, reducing your actual profit. Smart tax strategies ensure you keep as much of that gain as legally possible.

The Basic Rules

- You owe taxes only when you sell an asset at a profit — not while holding it.

- Losses can offset gains, potentially lowering your tax bill.

- How long you hold an asset determines if it’s a long-term or short-term capital gain.

Quick Pros and Cons of Understanding These Taxes

| ✅ Pros | ❌ Cons |

|---|---|

| Helps you plan sales to reduce taxes | Complex rules can be confusing |

| Improves overall investing returns | Tax laws change frequently |

Key Takeaway

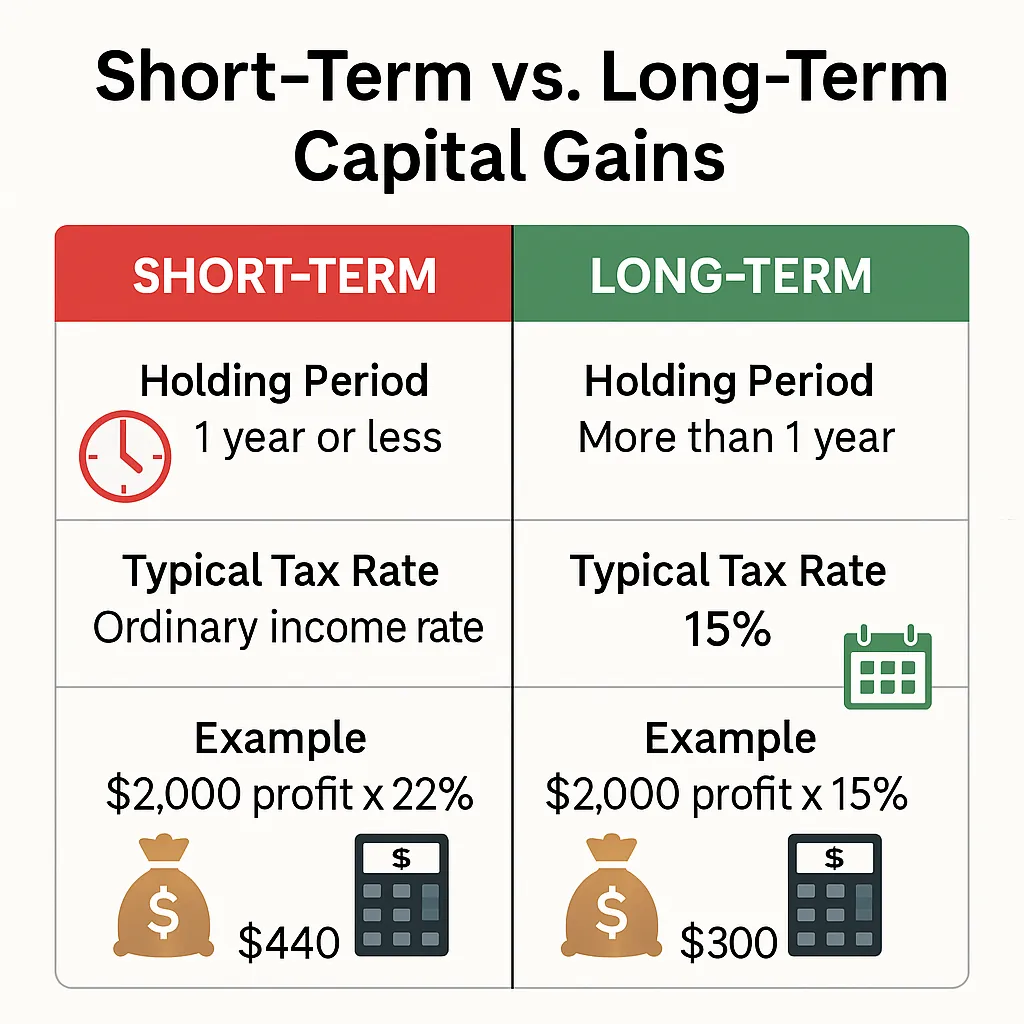

Short-Term vs. Long-Term Capital Gains

Not all capital gains are created equal. The tax rate you pay depends largely on how long you’ve held your investment before selling it. Understanding this difference can be the deciding factor between keeping hundreds or even thousands more in profit.

Short-Term Capital Gains

Short-term capital gains apply when you sell an investment you’ve held for less than one year. These gains are taxed as ordinary income, which means you could pay anywhere from 10% to 37% depending on your tax bracket. If you’re an active trader or day trader, this is a rate you’ll encounter often. For more on active trading strategies, see Best Day Trading Books.

Long-Term Capital Gains

Long-term capital gains apply when you sell an investment you’ve held for more than one year. These are generally taxed at lower rates — typically 0%, 15%, or 20% — offering a significant tax advantage. This is why many long-term investors avoid selling too soon.

Quick Pros and Cons

| ✅ Pros | ❌ Cons |

|---|---|

| Long-term rates are lower, saving you money | Holding too long could risk missing profit opportunities |

| Encourages patient, disciplined investing | Short-term gains can significantly reduce profit margins |

Detailed breakdown of capital gains tax rules and rates.

Tax Brackets, Rates, and How They Impact You

Your capital gains tax rate isn’t set in stone — it depends on your overall income and filing status. The IRS uses tax brackets to determine how much of your gains are taxed, meaning that a higher annual income often leads to a higher tax rate on your profits.

For a strategic approach to growing your investments while being mindful of taxes, you might find How to Invest Your Money Smartly for Long-Term Growth helpful.

Short-Term Capital Gains Rates

Short-term gains are taxed as ordinary income. That means they follow the same federal income tax brackets — currently ranging from 10% up to 37%. This can be a big hit if you’re a frequent trader or if you sell profitable investments too soon.

Long-Term Capital Gains Rates

Long-term rates are more favorable — typically 0%, 15%, or 20% depending on your taxable income. Investors in the lowest tax brackets can sometimes pay no federal tax at all on long-term gains, a powerful incentive to hold investments for over a year.

Example: $5,000 Gain in Different Tax Brackets

| Filing Status & Income | Short-Term Tax (Ordinary Income Rate) | Long-Term Tax Rate |

|---|---|---|

| Single, $40,000/year | 12% = $600 | 0% = $0 |

| Single, $100,000/year | 24% = $1,200 | 15% = $750 |

| Single, $300,000/year | 35% = $1,750 | 20% = $1,000 |

Official IRS guidelines on capital gains and losses, including current tax brackets and filing rules.

Strategies to Reduce Capital Gains Taxes

Taxes are a cost you can manage. With a few disciplined tactics, investors can legally minimize capital gains taxes and keep more profit after every sale.

1) Hold for > 1 Year When Possible

Crossing the one‑year mark can shift a sale from short‑term (ordinary income) to long‑term rates, which are generally lower. If your thesis is intact and risk is acceptable, patience often pays.

2) Use Tax‑Advantaged Accounts

Place frequently traded or high‑yield assets inside tax‑advantaged accounts when available (e.g., traditional or Roth IRAs). This can shelter growth from annual taxation. For account choice basics, see Roth IRA or Regular Brokerage Account.

3) Harvest Losses to Offset Gains

Tax‑loss harvesting means selling underperformers to realize losses that offset realized gains (mind the wash‑sale rules). It’s especially powerful for active traders balancing winners and losers. If you’re more active, compare approaches in Day Trading vs. Swing Trading.

4) Practice Asset Location

Place tax‑inefficient assets (frequent distributions or turnover) in tax‑advantaged accounts, and hold tax‑efficient, long‑term positions in taxable accounts. Over time, the compounding after‑tax difference can be substantial.

5) Donate or Gift Appreciated Shares

Donating long‑term appreciated stock to qualified charities can eliminate the capital gain while possibly providing a deduction (subject to rules). Gifting to family in lower brackets can also reduce family‑wide taxes (observe all annual exclusion and basis rules).

6) Time Your Sales Around Income Swings

Because long‑term capital gains thresholds are based on taxable income, realizing gains in a lower‑income year can lower the rate you pay. Consider spreading large sales across years when practical.

Quick Pros and Cons of Tax‑Efficient Tactics

| ✅ Pros | ❌ Cons |

|---|---|

| Lower effective tax rate on realized gains | Requires planning, record‑keeping, and discipline |

| Improves long‑term after‑tax compounding | Rules change; wash‑sale and basis rules can be tricky |

| Flexible: mix of timing, accounts, and offsets | May conflict with risk controls if you “wait for 1‑year” |

Looking for ideas that fit your risk tolerance while you plan around taxes? Review our insights on Penny Stock Alerts and how to manage volatility within a broader plan.

Practical tactics for minimizing realized gains, coordinating lots, and planning sales.

Real-Life Case Studies & Lessons Learned

Numbers on a chart are one thing — but nothing beats real stories when it comes to understanding the impact of capital gains taxes on investors’ bottom lines. Here are two scenarios that show how timing, strategy, and discipline can dramatically change after-tax outcomes.

Case Study 1: The Small Investor Who Kept More

Background: Alex, a part-time investor with a modest portfolio, bought $8,000 worth of growth stocks and sold them for $12,000 — a $4,000 gain. Instead of selling immediately, Alex waited until the one-year mark.

Outcome: By qualifying for the long-term capital gains rate of 15% instead of a 24% short-term rate, Alex saved $360 in taxes.

Lesson: Holding for the long-term not only aligned with market recovery but also reduced the tax bill, proving that patience really can pay.

Case Study 2: The High-Income Trader Who Paid the Price

Background: Jordan, a high-income earner, actively traded tech stocks throughout the year. In 2024, they realized $50,000 in short-term gains but also had $10,000 in losses from other trades.

Outcome: After offsetting the losses, $40,000 was taxed at Jordan’s 35% income tax rate — resulting in a $14,000 tax bill. Had Jordan held certain positions for over a year, the rate could have been 20%, reducing the tax owed by $6,000.

Lesson: Frequent short-term trading without tax planning can eat into net returns, even when portfolio performance looks good on paper.

How These Lessons Apply to You

- Think beyond price targets: Factor taxes into your exit strategy.

- Use loss harvesting: Offset gains before year-end to reduce tax impact.

- Align your holding period: Target long-term gains when possible.

For more on balancing risk and tax efficiency in a diversified approach, see our guide on Building a Diversified Stock Portfolio with $1,000.

Comprehensive breakdown of capital gains rules, rates, and strategies from a high-authority financial source.

Expert Insights on Capital Gains Planning

When it comes to minimizing capital gains taxes, professionals tend to agree on a few timeless principles: plan your exits, use the right accounts, and coordinate gains with losses. Below are distilled insights from tax practitioners and active market veterans to help you keep more of every win.

What Tax Pros Emphasize

“Your holding period is the first lever; documentation is the second. Keep meticulous lot records and plan sales a year ahead, not a week.” — CPA Insight

- Hold for long-term rates: When risk allows, crossing the 1‑year mark often lowers the bill.

- Harvest losses thoughtfully: Coordinate losers against realized winners; watch wash‑sale timing.

- Choose accounts wisely: Place high‑turnover ideas in tax‑advantaged accounts when available.

What Active Traders Focus On

“Tax efficiency matters — but never at the expense of risk management. Trim risk first, then optimize taxes.” — Trading Desk Perspective

Short‑term tactics can pair with tax planning if you’re disciplined. If you’re weighing approaches, compare styles in Day Trading vs. Swing Trading for fit and flexibility.

Practical Playbook (From the Pros)

- Pre‑plan exits: Put potential sale windows on your calendar 12+ months out.

- Stage sales: Break big disposals across tax years to manage bracket thresholds.

- Locate assets: Use IRAs/Roths for frequent trades; keep tax‑efficient core in taxable.

- Autopilot records: Turn on lot‑tracking and export realized gains/losses monthly.

- Sweep losses: Before year‑end, offset gains, then redeploy without triggering wash‑sales.

✅/❌ Expert Lens on Tax‑Efficient Planning

| ✅ Pros | ❌ Cons |

|---|---|

| Lower effective tax rate and higher after‑tax compounding | Added complexity: wash‑sale rules, lot accounting, timing windows |

| Aligns portfolio actions with annual tax thresholds | May conflict with urgent risk cuts or liquidity needs |

Want curated trade ideas and community perspective while you plan around taxes? Explore our Swing Trading Alerts for disciplined setups and risk frameworks that complement a tax‑aware strategy.

Actionable guidance on brackets, harvesting, and timing from a well‑regarded financial publisher.

Key Takeaways, FAQs & Final Thoughts

After diving deep into how capital gains taxes work, it’s clear that your after-tax return depends as much on strategy as it does on picking the right investments. Below, we’ll summarize the most important points, answer common questions, and give you the final push toward becoming a more tax-savvy investor.

Top 3 Key Takeaways

- Holding period matters: Long-term rates are almost always better than short-term rates.

- Plan your exits: Coordinate sales with your income levels and consider spreading gains over years.

- Use losses and accounts smartly: Offset gains, avoid wash-sales, and leverage tax-advantaged accounts.

Frequently Asked Questions

Do I pay capital gains tax if I reinvest the money?

No — reinvesting doesn’t avoid the tax. Once you sell and realize the gain, taxes are owed for that tax year, even if you put the money back into the market.

What if I have more losses than gains?

If your losses exceed your gains, you can use the excess to offset other income up to the IRS limit (currently $3,000 for individuals) and carry forward the rest to future years.

How often can I use tax-loss harvesting?

As often as you want, but be mindful of wash-sale rules that disallow losses if you repurchase a substantially identical security within 30 days before or after the sale.

To apply these tax-smart principles alongside winning trade ideas, see our latest Top Stock Alerts for potential opportunities that fit your risk and holding strategy.

Official guide to capital gains and losses, with real examples and tax planning tips from a top brokerage.

Final Thoughts

Investing isn’t just about picking winners — it’s about keeping more of what you earn. Whether you’re building a small portfolio or managing large trades, tax planning is a skill that pays for life. Treat every investment decision as both a market call and a tax decision, and you’ll be steps ahead of the average investor.

Further Resources & SEO Boost

To solidify your understanding of capital gains taxes and discover more strategies for tax-efficient investing, here are trusted resources from top financial authorities. These not only deepen your knowledge but also help you cross-reference the tactics we’ve covered in this guide.

Official IRS documentation covering definitions, rates, exemptions, and special rules.

Comprehensive overview from one of the world’s most recognized financial publishers.

Accessible and detailed explanation of capital gains taxes with real-world examples.

Practical advice for minimizing taxes and planning sales for maximum profit retention.

Explore More from TradeStockAlerts

- Penny Stock Alerts – Discover timely alerts for high-potential penny stocks.

- Swing Trading Alerts – Learn swing trading setups that align with tax efficiency.

- Top Stock Alerts – Get our best-performing trade picks delivered to your inbox.

By combining smart trading strategies with tax optimization and ongoing education, you position yourself to keep more of your profits year after year — an approach that pays dividends for decades.