The credit card debt crisis 20% APR is no longer a headline—it’s a household reality in 2025. As average credit card APR 2025 levels hover near (or above) the twenty-percent mark, balances snowball faster, minimum payments stretch budgets, and late fees compound the pain. This simple, practical guide explains how rising rates impact everyday families, why utilization and credit scores matter, and which payoff plans actually work. You’ll also get how to pay off credit card debt fast frameworks, credit score improvement tips, and a step-by-step plan you can start today.

💡 Key Points

- 📈 20% APR math: At today’s average credit card APR 2025 levels, interest grows quickly—small balances become big problems without a plan.

- 🧮 Payoff order matters: Avalanche (highest APR first) usually beats snowball on interest saved; combine with automatic extra payments.

- 🔄 Lower the rate: Negotiate APR, consider 0% balance transfer windows, or use a fixed-rate consolidation loan if it reduces total cost.

- 🪜 Score boosts: Fast wins come from lowering utilization < 30%, on-time payments, and removing errors—core credit score improvement tips.

- 🧭 Stay tactical: Set weekly micro-payments, cut recurring “leaks,” and track progress with a simple amortization checklist.

- 🔗 Go deeper: Explore diversification and side-income tactics via Day Trading vs Swing Trading, Penny Stock Alerts, and Diversified Crypto & Metals.

Market Overview: The U.S. Credit Landscape in 2025

The credit card debt crisis 20% APR gripping America in 2025 is more than a financial statistic—it’s a reflection of how rising interest rates and inflation have collided with stagnant wage growth. According to Federal Reserve data, total U.S. revolving credit surpassed $1.33 trillion in mid-2025, marking a record high. The average household now carries over $6,500 in credit card balances, a level unseen since the Great Recession. With rates pushing beyond 20%, even minimum payments barely dent principal balances, leaving consumers trapped in a cycle of compounding interest.

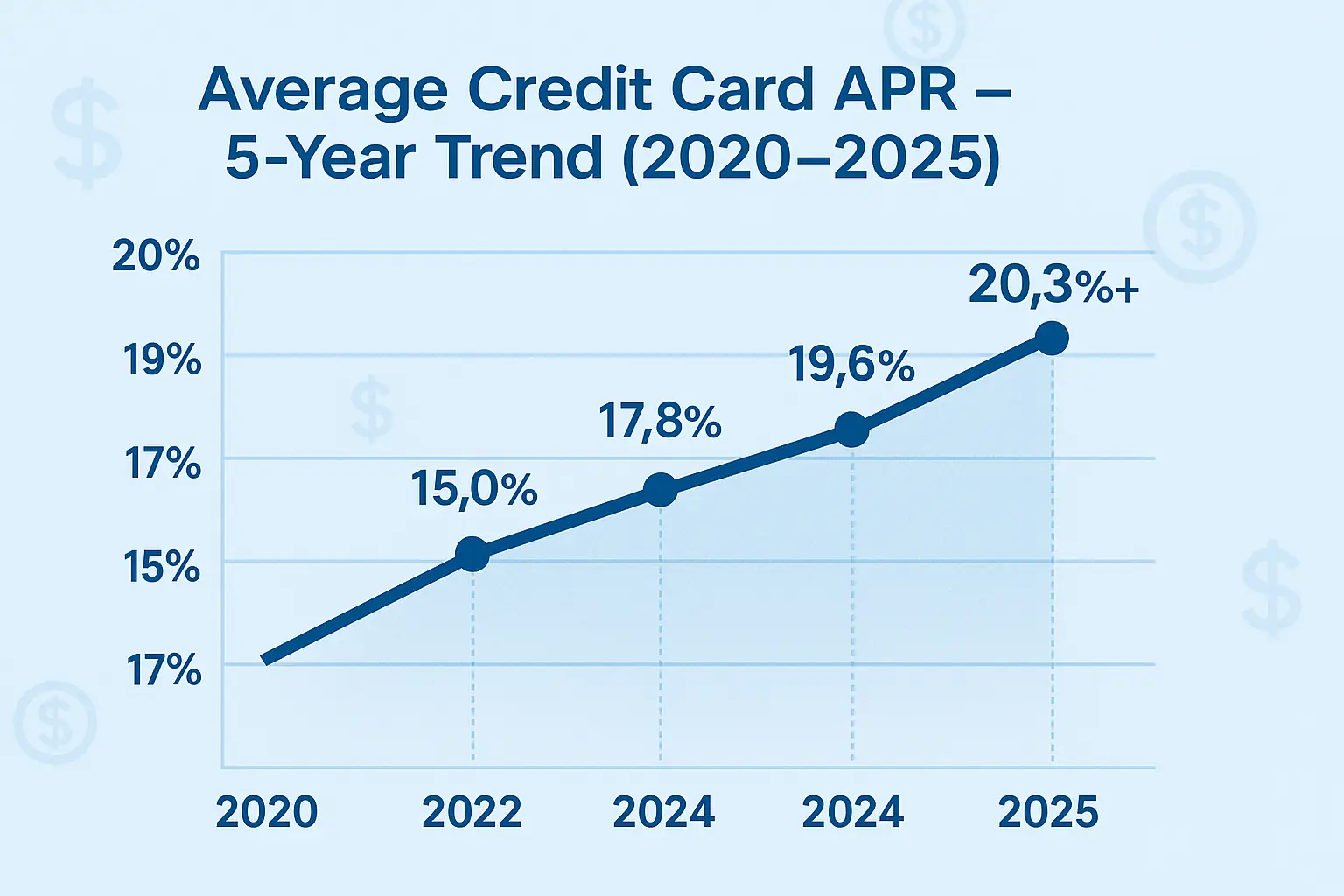

The average credit card APR 2025 has climbed to between 20.2% and 22.4% across major issuers like Capital One (COF), Discover (DFS), and American Express (AXP). Just three years ago, those averages hovered near 16%. This rapid escalation has reshaped how households manage monthly cash flow. Families that once viewed credit cards as temporary buffers are now facing hundreds—or even thousands—of dollars in annual interest costs.

Analysts from Yahoo Finance note that the combination of high inflation, higher-for-longer interest rates, and rising delinquencies has created a dangerous feedback loop. Borrowers spend more servicing debt, leaving less for savings or investing, which slows economic growth and increases financial strain. Lenders, in turn, tighten underwriting standards, creating a squeeze on both sides.

Meanwhile, balance transfer offers that once provided relief have become scarcer or shorter in duration, often lasting only six to nine months instead of a full year. The average introductory rate may still be 0%, but fees and shorter promotional periods erode the benefit. As a result, households trying to refinance credit card balances find it harder to escape high-interest debt even with disciplined payment strategies.

This chart comparison shows how major credit card issuers’ stock performance correlates with rising Treasury yields (10-year). As rates increase, banks’ net interest margins expand, benefiting their earnings—even as consumers face greater burdens. It’s a dual-edged sword: what helps lenders’ profits can simultaneously deepen the average American’s financial stress.

Credit card APR hikes also affect market sentiment. Financials (XLF) have outperformed broader indices like the S&P 500 in early 2025, while consumer discretionary stocks struggle. This divergence reflects how household spending patterns shift when debt service consumes a growing share of disposable income. Consumers delay big purchases, refinance fewer loans, and divert cash toward minimum payments—all of which slows GDP growth.

Warning Signs in the 2025 Credit Cycle

- ⚠️ Delinquencies Rising: 90-day late payments have ticked up to the highest level since 2011.

- 💳 Interest Burden: At 20% APR, a $6,000 balance accrues about $1,200 annually in interest alone.

- 🏦 Fed Policy: Despite cooling inflation, rate cuts remain slow—keeping APRs elevated.

- 📉 Consumer Confidence: Households report tighter budgets and lower savings, particularly among younger borrowers.

- 🧭 Financial Behavior: “Buy now, pay later” programs rise as short-term substitutes for maxed-out credit lines.

Ultimately, the data reveals a fragile ecosystem: consumers caught between elevated borrowing costs and persistent price pressures. But knowledge is leverage—understanding how credit conditions evolve is the first step toward escaping the cycle. In the next section, we’ll break down exactly how 20% APR interest compounds over time and show how to reduce its impact through structured payoff strategies and smart credit utilization.

How a 20% APR Turns Small Balances Into Big Problems

The credit card debt crisis 20% APR didn’t happen overnight. After years of rate hikes, the average credit card APR 2025 now sits near or above the twenty-percent line at many issuers, making carrying a balance dramatically more expensive. At 20% APR, interest accrues at roughly 1.667% per month. That means balances snowball unless you attack principal quickly.

Real-World Math (So You Can See It)

- 💳 $5,000 at 20% APR: monthly rate ≈ 1.667%. First-month interest ≈ $83.35. If your minimum is ~2% of balance ($100), only about $16.65 goes to principal at the start.

- 💳 $6,500 at 22% APR: monthly rate ≈ 1.833%. First-month interest ≈ $119.17. Pay the $130 minimum (2%), and just ~$10.83 reduces the principal initially.

This is why minimum-only payments can keep you stuck for years: most of the payment services interest, not principal. The fix is two-part—drop the rate and raise the principal portion of each payment.

What 20%+ APR Does to Household Budgets

- 📈 Payment drag: A larger share of income services interest, crowding out savings and investing.

- ⚠️ Utilization risk: High balances push credit utilization over 30%, hurting scores and raising future borrowing costs.

- 🔁 Refi squeeze: Shorter 0% transfer windows and higher fees make rollovers less effective than in prior years.

How to Pay Off Credit Card Debt Fast (Actionable Steps)

- Run the Avalanche: Pay minimums on all cards, then put every extra dollar to the highest APR card first. This saves the most interest versus snowball in high-rate environments.

- Automate weekly micro-payments: Four smaller payments a month reduce average daily balance and total interest.

- Lower the rate: Call to negotiate APR, or consider a 0% intro transfer if the fee & promo length truly cut total cost. Fixed-rate consolidation loans can work when the APR and term beat your current path.

- Drop utilization fast: Target < 30% on each card (and < 10% if possible) to support score gains—key for cheaper refi options.

- Cut recurring “leaks”: Audit subscriptions and high-cost habits; redirect those dollars to principal every payday.

For broader money strategy ideas while you’re digging out, explore: Day Trading vs Swing Trading (time vs. risk trade-offs), Penny Stock Alerts (know the risks before chasing returns), and our Diversified Crypto & Metals Portfolio Guide for long-term allocation thinking once high-interest debt is under control.

Data context and definitions: See the Federal Reserve for revolving credit trends, issuer/market coverage on Yahoo Finance, and practical payoff comparisons at NerdWallet and Forbes.

How Fed Policy and Inflation Fueled the Debt Spiral

The surge to a credit card debt crisis 20% APR didn’t happen in isolation—it’s the direct ripple effect of the Federal Reserve’s historic rate hikes from 2022 through 2024. While those hikes aimed to combat inflation, they also pushed consumer lending costs to record levels. The result: the most expensive credit environment in modern U.S. history. Today, households not only face higher grocery and housing prices, but they also pay a premium on every dollar borrowed.

When the Fed raised the federal funds rate above 5%, banks quickly passed those costs onto consumers through variable APR adjustments. Credit card interest rates—which move roughly in sync with prime—rose nearly point-for-point. The average American cardholder who carried $5,000 of revolving debt in 2020 paid around $750 in yearly interest. In 2025, that same borrower pays over $1,200 per year on the same balance.

This compounding pain creates a dangerous loop: higher interest eats disposable income → less spending slows growth → the Fed hesitates to cut rates → interest stays elevated → consumer debt deepens. This “credit drag” quietly suppresses economic momentum even when headline inflation cools.

The chart above illustrates how the Fed Funds Rate (blue) and the average credit card APR (red) have moved nearly in lockstep since 2022. This correlation reveals the “trickle-up” nature of monetary policy—decisions made in Washington ripple straight into household finances within weeks.

The Broader Economic Consequences

- 📉 Reduced consumer spending: With nearly one in three Americans carrying a revolving balance, higher interest costs reduce discretionary purchases—hurting retailers and small businesses.

- 💵 Increased defaults: Late payments are rising fastest among Gen Z and millennial borrowers, especially those holding multiple cards with variable rates.

- 🏠 Housing affordability squeeze: As consumers struggle with credit cards, they delay mortgage approval or refinancing, slowing real estate demand.

- 🧾 Wealth gap widening: Higher-income households can pay off cards monthly and benefit from interest-bearing savings, while lower-income families absorb compounding costs.

- ⚙️ Corporate credit tightening: Lenders increase reserves and raise standards, leading to fewer approvals for borderline borrowers.

Meanwhile, inflation may have cooled from its 2022 peaks, but service-sector prices remain sticky. Rent, insurance, and utilities still climb faster than wages for many families. As consumers allocate more income toward debt repayment, overall economic growth decelerates.

In a recent Federal Reserve report, policymakers acknowledged that the “credit squeeze” has become a dominant factor in consumer confidence readings. More Americans now cite debt stress as a top financial concern—surpassing inflation itself for the first time in a decade.

Investor Perspective: When Debt Becomes a Macro Signal

For investors, rising delinquencies and shrinking disposable income act as early-warning signals for broader market rotations. In 2025, that has meant a pivot away from consumer discretionary stocks and toward defensive sectors—utilities, healthcare, and gold miners. These asset classes historically outperform when consumer credit tightens.

Understanding the relationship between interest rate policy and credit strain helps traders anticipate volatility spikes. As short-term rates remain elevated, investors might look toward longer-duration bonds, defensive ETFs, and inflation-sensitive metals. Our Diversified Crypto Metals Portfolio Guide breaks down how metals and stable digital assets can hedge portfolios against debt-driven slowdowns.

Next, we’ll shift focus from policy to people—exploring how individual households can break free from high-interest cycles through structured payoff strategies and credit score optimization.

Practical Solutions: How to Pay Off Credit Card Debt Fast in 2025

If you’re caught in the credit card debt crisis 20% APR environment, the key isn’t panic—it’s a structured strategy. Many consumers underestimate how quickly a plan can shift momentum. By combining payoff prioritization, small behavioral tweaks, and smart use of promotional rates, you can significantly reduce interest and regain financial control.

1️⃣ Choose Your Payoff Framework

Two common methods dominate debt payoff: the Avalanche and the Snowball. The Avalanche method targets the highest APR first, minimizing total interest paid. The Snowball focuses on smallest balances first for psychological wins. In a 20% APR environment, the Avalanche usually saves more money—especially if combined with weekly micro-payments.

2️⃣ Automate Consistency and Track Progress

- 💰 Weekly payments: Break one large monthly payment into four smaller ones. This lowers your average daily balance and cuts total interest.

- 📊 Debt tracker apps: Use tools like NerdWallet or spreadsheet templates to visualize progress.

- ⚙️ Auto-draft setup: Link your checking to ensure never missing a minimum—payment history counts for 35% of your FICO score.

3️⃣ Lower the APR You’re Paying

At 20%+, negotiation is worth your time. Call your card issuer and request a review—if you have a clean record of on-time payments, they may reduce your APR by 2–4 points. Consider 0% balance transfer cards cautiously—calculate if the transfer fee (3–5%) offsets savings. Alternatively, a fixed-rate personal loan can consolidate multiple cards into one predictable payment.

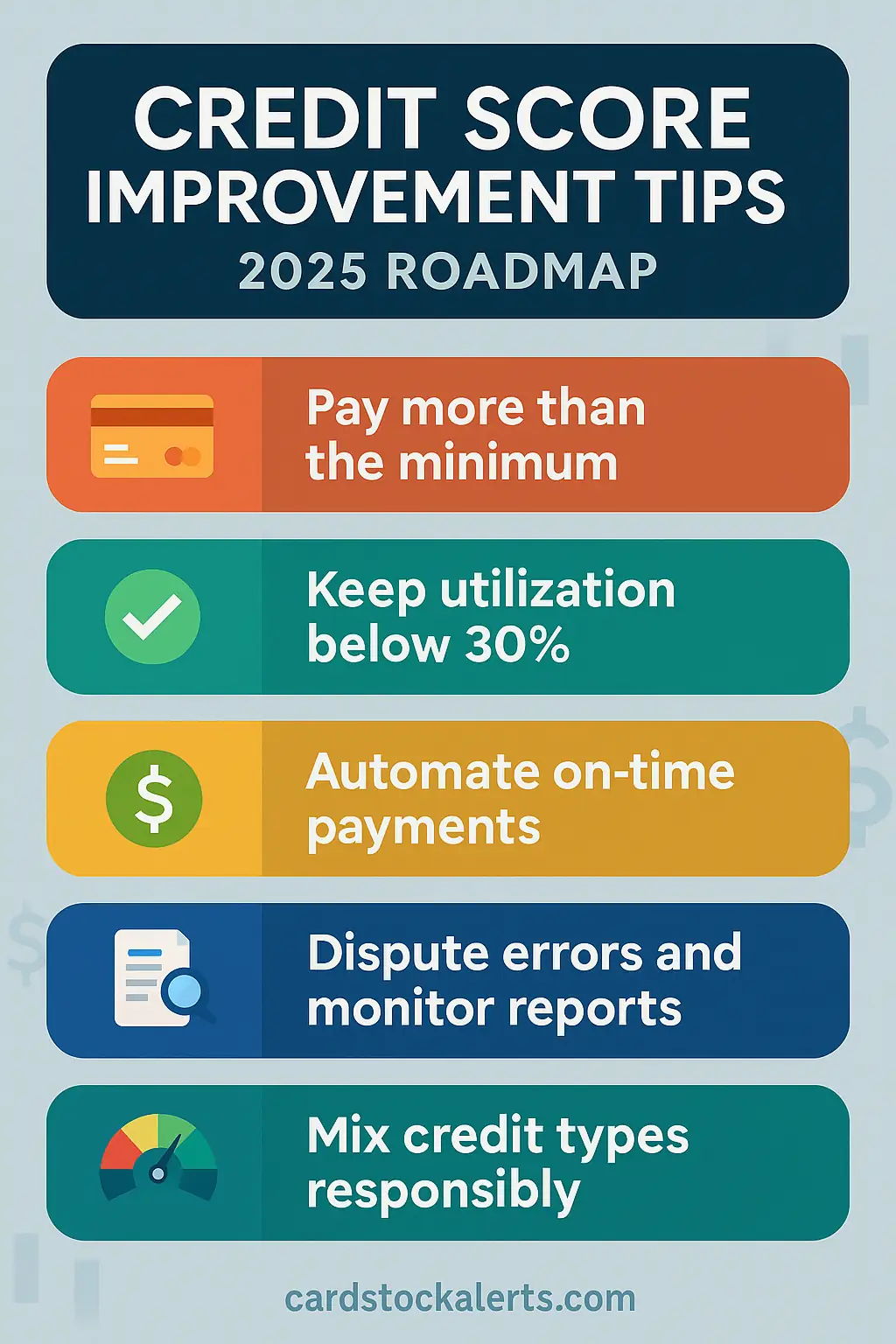

4️⃣ Optimize Your Credit Score for Cheaper Refinancing

- 📈 Keep utilization under 30%: Under 10% is even better for fast score gains.

- 📅 Pay before statement close: This lowers reported balances to bureaus.

- 🧾 Dispute errors: Review free reports quarterly for inaccuracies that drag down your score.

- 🔄 Diversify accounts: A small installment loan or secured credit card helps build mix, aiding future approval odds for consolidation products.

5️⃣ Grow Out of the Debt Cycle

Once balances drop, redirect that monthly payment amount into investments or savings to keep momentum. Even small investments—like learning low-risk trading in our Day Trading vs Swing Trading guide, or diversifying with metals and digital assets from our Diversified Crypto Metals Portfolio Guide—can turn previous interest payments into productive capital.

Many households discover that discipline, not income, makes the biggest difference. By cutting unnecessary subscriptions, dining costs, or impulse purchases, the freed-up funds can accelerate payoff speed dramatically. Combined with improved credit habits, this ensures not only debt reduction but also long-term access to cheaper borrowing rates and financial freedom.

Key Takeaways for 2025 Debt Relief

- 💳 Paying minimums isn’t progress—target the highest APR balance first.

- 📈 Weekly payments reduce compounding faster than monthly cycles.

- 💬 Negotiating your APR can save hundreds annually.

- 🧭 Lower utilization = higher credit score = lower future rates.

- 💡 Treat payoff like an investment in your net worth—not an expense.

The path out of credit card debt isn’t easy, but it’s measurable. With small, consistent changes and clear tracking, you can reclaim control—even amid a 20% APR landscape. In the final section, we’ll answer the most common questions about refinancing, score building, and protecting your financial stability in 2025.

Frequently Asked Questions (FAQ)

❓ What is the average credit card APR in 2025?

According to the Federal Reserve, the average credit card APR 2025 ranges from 20.2% to 22.4%, depending on credit tier. That means for every $5,000 balance, borrowers pay roughly $1,000–$1,200 per year in interest if they only make minimum payments.

💸 How can I pay off credit card debt fast?

Use the Avalanche Method—focus extra payments on your highest APR card first. Automate weekly payments to lower average daily balance, and negotiate lower APRs. Consider a 0% balance transfer or personal consolidation loan if it truly reduces total cost.

📈 How does a 20% APR affect my long-term finances?

At 20%, your balance doubles in about 3.5 years if unpaid. That high rate limits cash flow, weakens savings, and often depresses credit scores due to high utilization. Paying above the minimum and reducing utilization below 30% are essential steps.

🔄 Will the Fed lower interest rates soon?

While inflation has cooled, the Fed remains cautious. Analysts from Yahoo Finance suggest that rate cuts may begin in late 2025, but credit card APRs typically lag policy moves by several months.

💳 Can improving my credit score reduce my APR?

Yes. A higher score often qualifies you for better promotional offers and lower fixed rates. Focus on on-time payments, lower utilization, and disputing errors—these three habits can improve your FICO score by 30–80 points within months.

Final Thoughts: Building Financial Strength Amid High Rates

The credit card debt crisis 20% APR is a wake-up call for millions of Americans. While the current lending climate is challenging, it’s also an opportunity to reframe personal finance around discipline, planning, and smart credit management. No single strategy eliminates debt overnight—but consistency, automation, and informed decision-making compound faster than interest ever could.

As you improve your financial footing, remember that building wealth requires more than just reducing liabilities. It involves reallocating former debt payments into savings, investments, and diversification. Our Diversified Crypto Metals Portfolio Guide explains how to transition from paying interest to earning returns through a balanced, inflation-protected portfolio.

Stay proactive, track progress monthly, and celebrate small wins—those milestones keep you motivated long after your last balance is paid off. Financial freedom starts not with wealth, but with awareness and a clear plan.

Pauline Lei

Market analyst and lead writer at TradeStockAlerts.com. Pauline helps readers understand how interest rate cycles, inflation, and consumer credit trends influence household wealth, market dynamics, and long-term investing decisions. Her mission is to translate complex financial shifts—like the 20% APR credit crunch—into clear, actionable guidance for everyday investors.